All Categories

Featured

Table of Contents

- – Monetary Realities for Households in Yonkers N...

- – The Mechanics of Financial Obligation Settleme...

- – Legal Reset by means of Chapter 7 Personal ba...

- – Comparing Credit Report Effects

- – The Function of Nonprofit Credit Therapy

- – Navigating the Decision in Yonkers New York De...

- – Future Outlook for Financial Obligation Relief

Monetary Realities for Households in Yonkers New York Debt Relief Without Filing Bankruptcy

The economic climate of 2026 has presented an unique set of obstacles for customers. With interest rates remaining at levels that make bring revolving financial obligation pricey, lots of individuals find their regular monthly payments consume an increasing share of their non reusable earnings. When the expense of living in the surrounding area outmatches wage growth, the search for a viable exit from high-interest responsibilities ends up being a concern. Two main paths exist for those dealing with insolvency: financial obligation settlement and Chapter 7 bankruptcy. While both objective to fix financial distress, the systems, legal protections, and long-lasting consequences vary substantially.

Picking in between these choices needs a clear understanding of one's financial position and the specific guidelines governing debt relief in the local region. Financial obligation settlement includes working out with lenders to accept a lump-sum payment that is less than the total amount owed. On the other hand, Chapter 7 bankruptcy is a legal procedure that liquidates non-exempt properties to pay financial institutions, after which most unsecured financial obligations are released. Each approach has specific requirements and varying effects on an individual's ability to access credit in the future.

The Mechanics of Financial Obligation Settlement in 2026

Financial obligation settlement frequently attract those who want to prevent the viewed preconception of insolvency. The procedure usually starts when a debtor stops paying to their creditors and instead deposits those funds into a dedicated savings account. As soon as enough capital has actually accumulated, settlements begin. Lenders, seeing that the account remains in default, might be more happy to accept a partial payment instead of run the risk of getting absolutely nothing through an insolvency filing. Continuous interest in Debt Relief shows a growing need for alternatives to conventional insolvency.

Negotiating settlements is not without risk. Due to the fact that the process requires the debtor to stop making routine payments, late fees and interest continue to accumulate, frequently triggering the balance to swell before a deal is reached. Creditors are under no legal responsibility to settle, and some may select to pursue litigation instead. If a lender in Yonkers New York Debt Relief Without Filing Bankruptcy files a lawsuit and wins a judgment, they may be able to garnish salaries or place liens on property. Furthermore, the Irs normally views forgiven debt as taxable earnings. An individual who settles a $20,000 debt for $10,000 might receive a 1099-C type and be required to pay taxes on the $10,000 "gain," which can create an unforeseen tax expense the list below year.

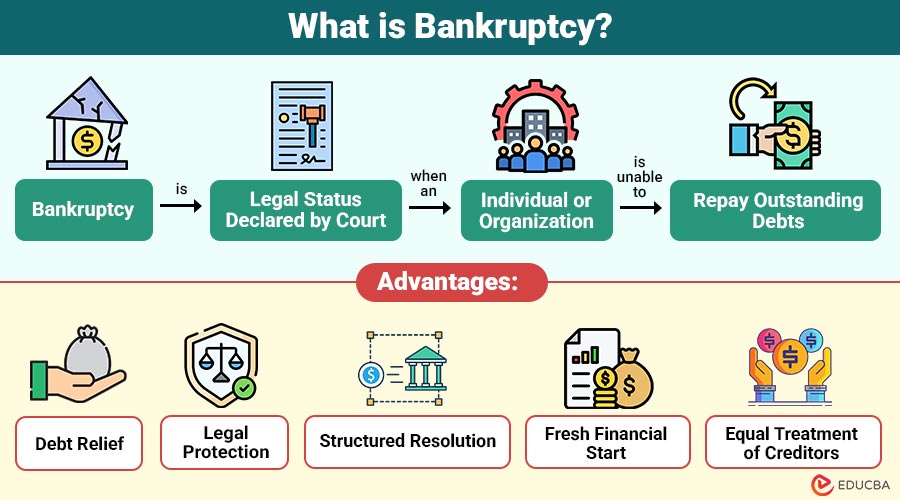

Legal Reset by means of Chapter 7 Personal bankruptcy

Chapter 7 personal bankruptcy offers a more formal and lawfully protected course. Typically called liquidation personal bankruptcy, it is developed to provide a "fresh start" to those with restricted income who can not reasonably anticipate to pay back their debts. To qualify in 2026, petitioners need to pass a methods test. This test compares their monthly earnings to the mean earnings for a home of their size in their specific state. If their earnings is below the average, they generally qualify. If it is above, they must supply in-depth info about their expenses to prove they lack the methods to pay a portion of their financial obligation through a Chapter 13 repayment plan.

One of the most instant advantages of filing for personal bankruptcy is the automatic stay. This legal injunction stops almost all collection actions, including telephone call, letters, suits, and wage garnishments. For lots of living in the United States, this time out offers immediate psychological relief. The process involves a court-appointed trustee who examines the debtor's assets. While lots of properties are exempt-- suggesting the debtor can keep them-- non-exempt home can be offered to repay financial institutions. Exemption laws vary by location, so the amount of equity one can keep in a home or automobile depends upon the statutes in the local jurisdiction.

Comparing Credit Report Effects

Both financial obligation settlement and Chapter 7 personal bankruptcy outcome in considerable damage to a credit history, however the timelines vary. A Chapter 7 filing stays on a credit report for 10 years from the date of filing. Debt settlement, because it involves marking accounts as "gone for less than the full balance," also hurts the score, though the private accounts typically fall off 7 years after the initial delinquency. Since settlement requires the debtor to purposefully fall behind on payments, the score often drops before the settlement even happens.

Healing is possible in both scenarios. Many individuals find that their credit report begins to improve within a few years of a Chapter 7 discharge since their debt-to-income ratio has enhanced so dramatically. By 2026, credit rating designs have become more sophisticated, yet the fundamental principle remains: lenders desire to see a history of on-time payments. Yonkers Debt Relief Programs has become a frequent subject for those dealing with collection calls. Whether one picks settlement or bankruptcy, the course to a higher rating includes restoring with secured credit cards and keeping small, workable balances.

The Function of Nonprofit Credit Therapy

Before a person can apply for insolvency in 2026, they are legally required to complete a pre-bankruptcy therapy session with a U.S. Department of Justice-approved firm. These firms, such as APFSC.ORG, supply an objective take a look at the debtor's scenario. A therapist evaluates earnings, costs, and debts to identify if a less drastic procedure may work. One such alternative is a Debt Management Program (DMP) In a DMP, the firm negotiates with creditors to lower rates of interest and waive costs. The debtor then makes a single regular monthly payment to the company, which distributes the funds to the creditors. Unlike settlement, the full principal is generally paid back, which can be less harmful to a credit report in time.

Nonprofit agencies also provide monetary literacy education and real estate therapy. For house owners in Yonkers New York Debt Relief Without Filing Bankruptcy who are stressed about foreclosure, HUD-approved real estate counseling is a vital resource. These services help individuals comprehend their rights and explore choices like loan adjustments or forbearance. Since APFSC.ORG is a 501(c)(3) not-for-profit, the focus remains on education instead of profit, offering a contrast to for-profit debt settlement companies that might charge high upfront fees.

Navigating the Decision in Yonkers New York Debt Relief Without Filing Bankruptcy

The choice in between settlement and insolvency frequently comes down to the nature of the financial obligation and the debtor's long-term objectives. If the majority of the financial obligation is owed to a couple of creditors who have a history of negotiating, settlement might be a quicker path. If the financial obligation is spread out across several loan providers or if there is an active risk of wage garnishment, the legal protections of Chapter 7 are often more effective. Customers often look for Debt Relief in Yonkers when handling high-interest balances.

Home ownership is another major aspect. In various regions, the homestead exemption determines how much home equity is secured in bankruptcy. If a resident has significant equity that surpasses the exemption limit, a Chapter 7 filing could result in the loss of their home. In such cases, debt settlement or a Chapter 13 reorganization may be the only methods to deal with financial obligation while keeping the property. Expert guidance stays a concern for individuals looking for relief throughout financial difficulty.

Future Outlook for Financial Obligation Relief

As 2026 advances, the legal environment surrounding debt relief continues to evolve. New regulations on for-profit settlement companies have increased openness, yet the core threats stay. Insolvency courts in the regional district have moved toward more digital procedures, making filings more efficient but no less severe. The 180-day pre-discharge debtor education requirement stays a foundation of the procedure, guaranteeing that those who receive a discharge are much better equipped to handle their finances in the future.

Financial distress is hardly ever the outcome of a single choice. It is often a mix of medical emergencies, task loss, or the relentless pressure of inflation. By analyzing the differences between settlement and bankruptcy, citizens in Yonkers New York Debt Relief Without Filing Bankruptcy can make a decision based upon data rather than fear. Looking for a totally free credit counseling session through a DOJ-approved not-for-profit is frequently the most productive first action, as it provides a clear view of all offered choices without the pressure of a sales pitch.

{kind=link}

Table of Contents

- – Monetary Realities for Households in Yonkers N...

- – The Mechanics of Financial Obligation Settleme...

- – Legal Reset by means of Chapter 7 Personal ba...

- – Comparing Credit Report Effects

- – The Function of Nonprofit Credit Therapy

- – Navigating the Decision in Yonkers New York De...

- – Future Outlook for Financial Obligation Relief

Latest Posts

Why Nonprofit Status Matters for Regional Financial Obligation Assistance

Changing Your Financial Life With Credit Counseling

Homeownership Success Starts with Financial Education in Columbus Credit Counseling

More

Latest Posts

Why Nonprofit Status Matters for Regional Financial Obligation Assistance

Changing Your Financial Life With Credit Counseling

Homeownership Success Starts with Financial Education in Columbus Credit Counseling